The interest rates are at minimal levels in the whole of Europe (and not only), that there is very creates many difficulties for european banks, since it removes a source of income in the core. However, in the Portuguese case, in particular, the difficulties may become more acute if, while maintaining rates at low levels, the interest rates of the public debt Portuguese improved a result of the risks internal, external, or both. The warning is from the Bank of Portugal, in the most recent edition of the Financial Stability Report, which points to this factor of uncertainty as one of the major risks able to worsen the vulnerability of domestic banks.

The business model of the Portuguese banks, like other european banks, is particularly sensitive to the environment of prolonged low interest rates. These vulnerabilities hinder the generation of results and, therefore, of capital, undermining the perception of the sector among investors, either for the purpose of capital reinforcement (for current and/or potential new private shareholders), either for the placement of debt in the wholesale financial markets".

This is a general consideration on the part of the Bank of Portugal, to look forward and to look at the possibility of banks having to go to the market in the medium term, either through the raising of capital whether through debt issues on a regular basis. For now, however, the "perception of the sector among investors" seem to live days on the best, since that "in the last few months, if you found interest on the part of private investors to enter or increase their involvement in domestic banking groups". The recent cases of BPI (CaixaBank) and of the BCP entry (Fosun) are the concrete cases, in addition to the sale in the course of the New Bank.

The Bank of Portugal’s perspective, however, risks and vulnerabilities — some more likely than others — that may be factors of destabilization. And here, the institution led by Carlos Costa, shows itself particularly concerned with the risk of a rise of the interest rates of Portuguese public debt, something that the rest has already been checked in the last few weeks. Here’s what it says in the institution, in Financial Stability Report:

A reassessment of risk premia, to materialize, will affect across the entire financial system, either through the effect of the devaluation of the exposures to financial assets, or increasing the cost of financing.

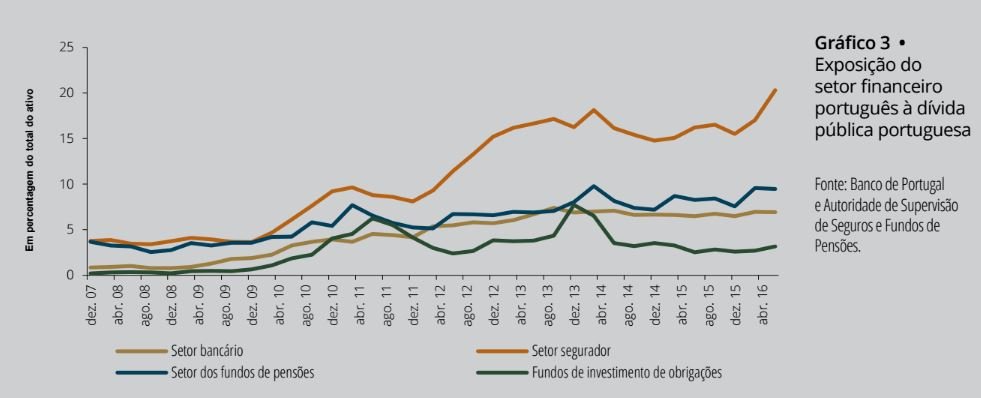

banks, insurance companies and pension funds in Portugal have a "significant exposure to the sovereign debt situation in fact common to many other european countries – by which these institutions would be particularly affected by a further increase in risk premiums and the corresponding depreciation of these assets," adds the Bank of Portugal.

After the volatility that marked the year of 2016 in the financial markets and factors of uncertainty such as Brexit and the victory of Donald Trump in the U.S., the Bank of Portugal warns that the national authorities should do their role. "If it is true that external developments are outside the control of the resident entities, it is important that the factors and idiosyncratic, on which there is the capacity to act, continues to evolve favorably, in order to ensure the maintenance of confidence of the investors in the evolution of national public finances," says the institution.

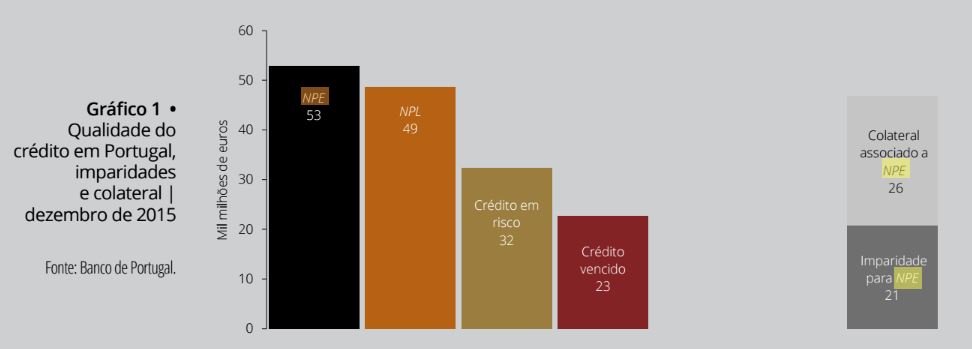

Among the other risks to the banking national, several times repeated by the Bank of Portugal and by other institutions, are the burden of the assets do not generate income (such as credit risk, especially in companies) and that they catch the new credit.

In the Financial Stability Report, the Bank of Portugal quantifies these exhibits are not income-generating in 53 billion, and there are 21 thousand million in impairments carried out, and 26 thousand million in guarantees.

The Bank of Portugal explains that "the values of overdue credit, credit risk or NPL/NPE net of impairments may not be interpreted as a loss is certain or almost certain to the banks". However, these are exhibits that in several countries in Europe have led investors to focus on risk that the banks have in their balance sheets.

at The european level, it is necessary to define and adopt measures that accelerate the reduction of the stock of non-performing loans in the balance sheet of the banks; these measures should have a multidimensional nature and to meet the national specificities of these exhibitions, the constraints of profitability and capital of banks, the regulatory environment is more demanding and the potential systemic consequences associated with exposures shared by multiple institutions in the banking system.

in addition, the Bank of Portugal warns of the need for the national banks to continue to reduce costs, not only to respond to low interest rates as, also, the other challenges such as the digital and demographic changes.

To cope with the constraints that the environment of low interest rates puts to the generation of results, credit institutions shall make a re-evaluation comprehensive of their business models and cost structure, which takes into account the challenges arising from demographic developments and the opportunities and challenges arising from the digitization of the banking business".

The Bank of Portugal mentions, still, as risks less likely the risk of low interest rates increase the probability of no sale, on the part of the banks, "products not suitable to the risk profile of their retail customers", at a time that is a given that there are "pressures regulations that oblige the banks to the issuance of debt instruments and capital".

Finally, you can, also, there is a risk of falling prices in the real estate, which visit the banks, for several possible reasons: for example, the reasons "associated with the deterioration of economic conditions, tax changes or an eventual rapid decrease of the exposure of the financial sector, this type of assets", that is, a situation in which multiple agents if they see the need to sell, flooding the market for this type of assets.

No comments:

Post a Comment